As your loved ones get older, you’ll notice that regular checkups, medications, and unexpected hospital visits become more frequent and more expensive.

This guide walks you through everything you need to know about health insurance for senior citizens, including how it works, what it covers, and how to choose a plan that offers real value and long-term protection for your loved ones.

Why health insurance for senior citizens matters

Medical bills rise sharply as your parents age. A doctor’s visit, specialist care, or emergency hospitalisation can easily cost hundreds of thousands of naira. If you are outside the country, there is the added worry of not being able to be physically present for support. Without health insurance for senior citizens, these costs can derail your finances.

Consider these realities:

A simple doctor’s consultation at a private hospital can cost anywhere between ₦10,000 and ₦30,000, depending on the hospital. If your parents need to see a specialist for diabetes, hypertension, or arthritis conditions that require regular monitoring, you’re looking at monthly medical expenses of ₦50,000 to ₦150,000, and that’s before medications, lab tests, or any procedures.

Hospital admission for a senior with a health emergency can easily reach ₦500,000 to ₦2 million within days. A hip replacement surgery costs upwards of ₦3 million. Dialysis sessions for kidney disease run anywhere from ₦50,000 to ₦150,000 per session, and are needed multiple times weekly. Cancer treatment can cost more than ₦10 million. So you see that the costs stack up.

The emotional toll is just as heavy. You’re trying to build your own life, support your own family, plan for your children’s future, yet you’re constantly bracing for the next medical emergency from home. The guilt when you can’t send enough. The fear when your phone rings unexpectedly. The exhaustion of being the family’s healthcare safety net.

Here’s what health insurance for senior citizens actually does:

It transforms unpredictable, crushing medical costs into manageable, predictable premiums. With the right seniors plan, your parents can walk into hospitals and get care without paying up front. Their medications are covered or heavily subsidised. Routine check-ups happen regularly instead of being avoided due to cost. Some plans even cover health insurance for pre-existing conditions, assuring you that nothing is left out.

Most importantly, it gives you peace of mind. You’re no longer wondering if you can afford the next medical crisis. With convenient options to buy health insurance for your parents online, you can put a system in place that actually works.

Understanding health insurance for senior citizens: Key differences

Not all health insurance works the same way for older adults. If you’ve been researching seniors’ health insurance plans in Nigeria, you’ve probably encountered confusing terms, conflicting information, and policies that seem designed to exclude rather than include your parents.

Let’s break down exactly what makes health insurance for senior citizens different:

- Age limits and eligibility

Most standard plans stop accepting new members over 60-65, while health insurance for elderly parents is designed for 50-75+ and recognises that seniors need more frequent, tailored care.

- Pre-existing conditions coverage

This is where many families hit a wall. Your parents likely has diabetes, hypertension, arthritis, or other chronic conditions that developed over the years. Standard plans often exclude pre-existing conditions, impose long waiting periods, or charge much higher premiums. The right health insurance for senior citizens recognises these conditions and provides coverage from day one or after a short waiting period

- Waiting periods

Waiting periods are the time between when you purchase a policy and when certain benefits become active. For seniors, this is critical:

- Immediate coverage: Accidents and emergencies (usually 24-48 hours after activation)

- Short waiting periods: Outpatient consultations and basic care (typically 30 days)

- Longer waiting periods: Major surgeries and specific treatments (90 days to 12 months)

- Pre-existing condition waiting periods: Can range from 0 to 12 months, depending on the provider and condition

Understanding all these nuances can feel overwhelming, especially when you’re trying to make sure your parents get the care they deserve. That’s why having a plan that’s specifically designed for senior citizens can make all the difference.

With SendCare by MyCoverGenius, you can find coverage that recognises the unique needs of older adults, covering pre-existing conditions, and ensuring your parents have access to care when they need it most. This way, you will have peace of mind, knowing they’re protected without the confusion or exclusions of standard plans.

What the right seniors’ plan should typically cover

When comparing elderly health plans in Nigeria, some benefits are essential. Here’s what every health insurance for senior citizens should cover, along with optional extras that can add real value.

| Coverage type | Why it’s critical for senior | What to look for (minimum affordable standards) |

| Inpatient hospital care | High risk for surgeries, infections, heart issues, and emergencies. | A reliable annual limit of at least ₦1,000,000 for hospital admissions, including emergency surgeries and access to a Semi-Private Ward. |

| Outpatient consultations | Regular doctor visits for chronic disease monitoring are essential for senior health management. | A minimum annual limit of ₦600,000 for general consultations and guaranteed access to specialists (e.g., at least twice/month). |

| Prescription medications | Most seniors take daily medications for chronic conditions. | A minimum pharmacy limit of ₦150,000 per annum, with specific, dedicated coverage for chronic disease medications (e.g., at least ₦100,000 per annum). |

| Chronic disease management | Diabetes, hypertension, arthritis, and heart disease require ongoing monitoring and treatment. | Explicit coverage for chronic conditions and all necessary regular monitoring tests |

| Diagnostic tests & imaging | Needed for diagnosis and monitoring. | Comprehensive diagnostic coverage up to the outpatient limit, including essential advanced investigations like CT/MRI/Echo twice per year. |

| Emergency care | Immediate access saves lives. | Full coverage for 24/7 emergency room access, ambulance services, and emergency stabilisation (including radiological/lab investigations) up to a minimum of ₦100,000 per annum. |

| Rehabilitation care | Essential for recovery from surgeries or managing mobility issues. | Inclusion of physiotherapy care with a minimum of 8 sessions/year. |

Highly recommended optional benefits

Beyond the essential coverage, some extras can make a real difference for your parents’ well-being without costing more than necessary.

- Optical care: Covers eye exams, glasses, and cataract surgery to manage age-related vision issues.

- Dental coverage: Basic care, extractions, and dentures help prevent small problems from becoming expensive.

- Home care services: Post-surgery support and physical therapy at home reduce the risk of rehospitalisation.

- Telemedicine / 24-hour doctor access: Quick virtual consultations for chronic condition check-ins.

- Medication delivery: Prescriptions delivered directly to your parent’s door within 24–48 hours.

- Wellness and preventive care: Annual screenings, cancer checks, and heart health assessments catch issues early. Elderly health plans in Nigeria often include these as optional extras.

The difference between standard and senior-specific coverage is the emphasis on chronic disease management and regular preventive care, the services older adults actually use most frequently.

How to assess your parents’ specific health insurance needs for seniors plan

Before comparing options, you need a clear picture of your parents’ health requirements.

- Start with their current health; chronic conditions like diabetes, hypertension, arthritis, or heart disease, regular medications, and any hospitalisations in the past year. Understanding these details helps you identify which coverage features are essential versus optional.

- Next, look at their lifestyle and healthcare usage. How often do they see doctors? Do they prefer private hospitals or public facilities? Can they travel easily, or do they need home-based care? If you’re abroad, consider whether coverage that works nationwide, or even internationally, would be important.

- Budget matters too. You want a plan that balances affordability with the coverage your parents actually need. A good seniors plan can cover chronic conditions, routine check-ups, and emergencies, while avoiding unnecessary extras. Taking the time to assess their health, lifestyle, and spending limits ensures you choose health insurance for your elderly parents that genuinely protects them and gives you peace of mind.

- It is also crucial to consider your family’s risk tolerance. What would happen if your parents needed emergency surgery next month? Could you manage a ₦2 million hospital bill without insurance or quickly access funds for an unexpected medical crisis? How would covering a major medical emergency affect your own financial stability?

These questions are not easy, but they matter. Health insurance for senior citizens is not just about the premiums you pay; it is about protecting your family from huge costs and giving you real peace of mind.

For comprehensive information on family health insurance, types of health insurance you can get for your family and coverage options, visit our guide on family health insurance in Nigeria.

Coverage details to watch out for in seniors’ health insurance plan

When comparing plans, there are a few important points to consider:

- Overall benefit limits: Some plans have yearly maximums. Make sure the plan provides enough coverage for your parents’ likely needs, especially if they have chronic conditions.

- Limits on specific services: A plan might cover general care well, but restrict certain treatments like surgeries or advanced procedures. Check what’s included so there are no surprises.

- Hospital access: Ensure the plan’s network includes quality hospitals near your parents. Nationwide coverage is only useful if they can actually reach the facilities.

- Co-payments and deductibles: Some plans require you to contribute to costs before coverage starts. Understand these out-of-pocket responsibilities so you’re prepared.

A senior’s plan that balances these points ensures your parents receive essential care, routine monitoring, and emergency protection without unexpected financial strain.

How SendCare simplifies finding the right coverage

Finding the right coverage for your parents can feel overwhelming. A lot of time is spent comparing policies, checking hospital networks, understanding exclusions, and deciphering complicated documents is exhausting.

SendCare simplifies this by bringing all three SendCare senior plans together in one platform, so you can see exactly what each plan offers and pick the one that fits your parents’ needs and your budget.

Here’s what makes each plan clear and practical:

- SeniorsPlan: Covers inpatient and outpatient care, general consultations, chronic condition treatment, and essential medications. It’s a great choice if your parents have routine healthcare needs.

- SeniorsPlan Plus: Adds higher outpatient limits, more pharmacy support, specialist visits, and additional procedures, which is ideal for seniors who need more regular monitoring or treatment for chronic conditions.

- SeniorsPlan Prime: The most comprehensive tier, including extensive inpatient coverage, advanced surgeries, physiotherapy, dental and optical care, telemedicine, wellness checks, renal dialysis and more for seniors with complex healthcare needs.

SendCare takes the guesswork out of health insurance, helping you pick a seniors plan that fits your parents’ needs and keeps you confident their care is covered.

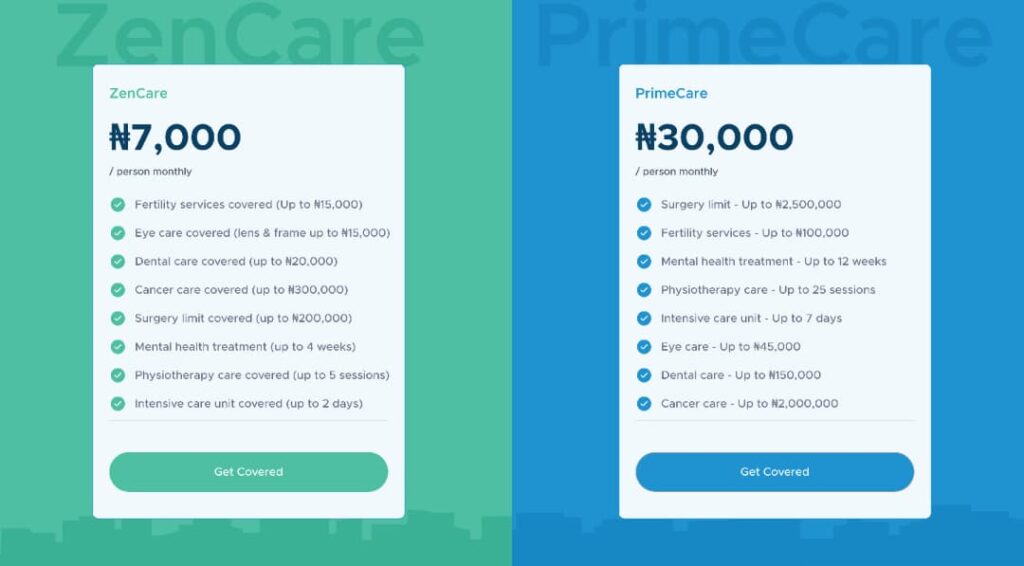

Compare senior health plans on SendCare

Step-by-step guide: How to buy elderly health insurance plans online using SendCare

You’ve assessed your parents’ needs. You understand what coverage they require. Now it’s time to secure a seniors plan that protects them, wherever you are in the world.

Here’s exactly how to do it, the simple way.

Step 1: Gather essential information

Before you start comparing plans, collect these details about your parent:

Personal information:

- Full legal name as it appears on official ID

- Date of birth

- Gender

- Residential address in Nigeria

- Contact phone number and email

Medical information:

- Known chronic conditions (diabetes, hypertension, arthritis, heart disease, etc.)

- Current medications and dosages

- Recent hospitalisations or surgeries in the past 12 months

- Known allergies

- Name and location of preferred hospital or doctor

Coverage Preferences:

- Desired coverage start date

- Budget range, either quarterly or annually

- Specific benefits needed based on your earlier assessment

- Whether other family members need coverage simultaneously

Payment Information:

- How you’ll pay (if you’re abroad: international card in USD/GBP/EUR; if you’re in Nigeria: local card or transfer)

- Billing is either by quarterly, bi-annual, or annual payment

Having this information ready will help you understand which seniors plan to buy for your parents or the elderly.

Step 2: Compare plans on SendCare

Finding the right health insurance for senior citizens doesn’t have to be stressful. SendCare simplifies the process so you can see all the best options in one place, without juggling multiple websites or phone calls.

Here’s how it works:

- Visit SendCare’s page at mycovergenius.com/sendcare

- Go to ‘plans’ and select ‘SeniorsPlan’.

- View curated options: SendCare presents 3 different seniors plan options tailored to your parents’ health profile.

What you’ll see for each plan:

- Annual maximums and any sub-limits

- Key benefits in simple terms

- Transparent pricing (quarterly/annual)

- Number and names of accessible hospitals near your parent

- Pre-existing condition coverage

- Prescription drug coverage details

To better understand what you’re paying for and why, read our comprehensive guide on HMO costs in Nigeria, which breaks down typical pricing across different coverage levels.

Step 3: Sign up and get your parents covered

Once you’ve picked the right seniors plan on SendCare, the next step is to set up your account and secure coverage.

- Start by creating a MyCoverGenius account. Since you’re signing up from outside Nigeria, enter your current location.

- Next, provide your personal details: first name, last name, date of birth, and gender.

- Finally, enter your email and WhatsApp number. These are needed to verify your account with a one-time password (OTP). Once verified, you’re ready to proceed with purchasing health insurance for your senior citizen and ensuring reliable elderly health plan coverage in Nigeria.

Step 4: Payment & policy delivery

Once you choose the right seniors plan for your parent, you pay in USD, GBP, or EUR using your international debit or credit card. No naira transfers, no local bank restrictions, no back-and-forth with relatives.

What happens after payment

- Immediate receipt: You get a payment confirmation by email instantly.

- Instant digital ID: The plan is created, and your parents’ e-HMO ID is generated automatically.

- Policy activation: Your parents’ seniors plan becomes active 24 hours after registration, after which they can walk into any hospital to receive care.

- Hospital network: A full list of all hospitals under their plan is accessible to your parents.

Why use SendCare to secure health insurance coverage for seniors

SendCare makes it simple for Nigerians in the diaspora to buy health insurance for senior citizens and elderly parents back home in Nigeria.

You already know your parents’ needs and the kind of elderly health plans in Nigeria that work for them. Here’s why SendCare is a great choice for your parents:

1. Simplifies the process

Trying to find the right health insurance for senior citizens on your own can be daunting and even confusing. Different providers have different age limits, waiting periods, pre-existing condition rules, and hospital networks. SendCare has plans that actually focus on covering seniors, letting you compare the best options quickly. And if you need help, you can easily reach out to us via a phone call and WhatsApp at 09070008899 so we can guide you in picking the right plan for your parents.

2. Perfect for Nigerians living abroad

If you’re overseas, coordinating insurance can be tricky. SendCare lets you buy health insurance for your parents online, pay in USD, GBP, or EUR, and manage everything from your phone or laptop. Your parents get coverage activated in Nigeria without complicated steps or paper forms.

3. Reliable and trustworthy

It’s normal to worry about insurance myths that might stop you from getting coverage for your parents. You may have heard things like “insurance companies never pay claims,” “insurance is only for rich people,” or “the claims process is deliberately complicated.” These concerns are real, but they don’t reflect the reality when you use SendCare.

SendCare works with licensed, reputable insurers and pre-vetted hospitals, so you can feel confident your parents’ coverage will actually work when needed. Every plan clearly shows what’s covered, and if issues arise, we guide you through the process so you aren’t left handling claims alone. This is how SendCare ensures your parents’ health insurance always works.

4. Plans designed for seniors

Standard policies often exclude pre-existing conditions or have long waiting periods, making them unsuitable for ageing parents. SendCare focuses on health insurance for elderly parents designed for chronic care, medications, and frequent check-ups.

5. Transparent pricing

Hidden fees, co-payments, or confusing limits can make a plan more expensive than it seems. SendCare shows upfront premiums, limits, and benefits clearly. You can compare all seniors plans side by side and pick what fits your parents and your budget.

Explore senior plans on SendCare now

Common questions about health insurance for senior citizens (FAQ)

What does MyCoverGenius health insurance for senior citizens cover?

MyCoverGenius health insurance for senior citizens plans, available through SendCare, cover inpatient care, outpatient consultations, specialist visits, prescription medications, diagnostics, emergency care, and management of chronic conditions like diabetes, hypertension, surgery, arthritis, etc. Optional benefits include optical care, dental coverage, 24/7 telemedicine, and others, depending on the plan tier.

How can I buy health insurance for my parents online?

Buying health insurance for your parents online through SendCare is simple. Select ‘seniorsplan’ here, enter age and location, compare curated plans with clear coverage and pricing, complete the application, and pay securely in USD, GBP, or EUR. Once registration is complete, your parents’ digital HMO ID is generated instantly, and they can start using their health insurance plan within 24 hours. The process only takes a few minutes, making it easy for Nigerians abroad to secure coverage for their elderly parents back home.

How do pre-existing conditions affect coverage for older adults?

Pre-existing conditions are health issues your parent had before enrolling in insurance and are a major concern. SendCare’s senior plans provide transparent coverage for pre-existing conditions, with short waiting periods and full benefits once active. Always disclose your parents’ medical history honestly to avoid claim issues. Common conditions include diabetes, hypertension, heart disease, arthritis, and asthma.

What are the best health insurance plans for seniors with chronic illnesses in Nigeria?

The best senior plans for chronic conditions cover pre-existing illnesses, regular outpatient visits, specialist consultations, medication benefits, and diagnostic tests. Top plans also include eye care, dental care, surgeries, and preventive screenings. All SendCare senior plans offer these features, with the main difference being the benefit limits. You can compare the plans on SendCare to find the limit that best matches your parents’ healthcare needs and budget, ensuring comprehensive coverage for their chronic conditions.

How long is the waiting period for senior citizen health insurance in Nigeria?

With SendCare, your parents’ senior plan coverage becomes active 24 hours after registration. This means they can start using their plan immediately after 24 hours.

What should I do if my parent needs emergency care?

Emergency care is available 24 hours after registration. Your parent can go directly to any hospital in the SendCare network. We recommend they first use the “Visit Hospital” feature on their HMO dashboard, as this helps track their arrival and ensures the hospital is ready.

They should present their digital HMO ID, which includes personal details and the HMO provider’s name. If there’s any confusion or support needed, you can reach out to us for help.

Which hospitals can my parents access with SendCare?

Your parents can access a wide network of hospitals across Nigeria, included in their SendCare senior plan. After registration, they’ll receive a digital HMO ID and a list of hospitals where their coverage is valid. This lets them receive care without delays, whether it’s a routine visit, specialist consultation, or emergency care.

Does the plan cover surgeries, eye care, dental care, and chronic illnesses?

Yes. All three SendCare senior plans cover chronic conditions, surgeries, eye care, dental care, and more. The main difference between plans is the benefit limit, so you can choose the plan that best fits your parents’ healthcare needs and budget.

Can I update my parents’ information or manage the plan remotely?

Yes. As the adult child managing coverage from abroad, you can handle everything online. Once your parents’ SendCare senior plan is active, you can update personal information, manage renewals, and monitor coverage from your dashboard. There’s no need for in-person visits in Nigeria.

Have questions? Our support team is available via phone at +234 9070008899 or visit mycovergenius.com/sendcare for more information about senior health insurance options and how we can help protect your loved ones.